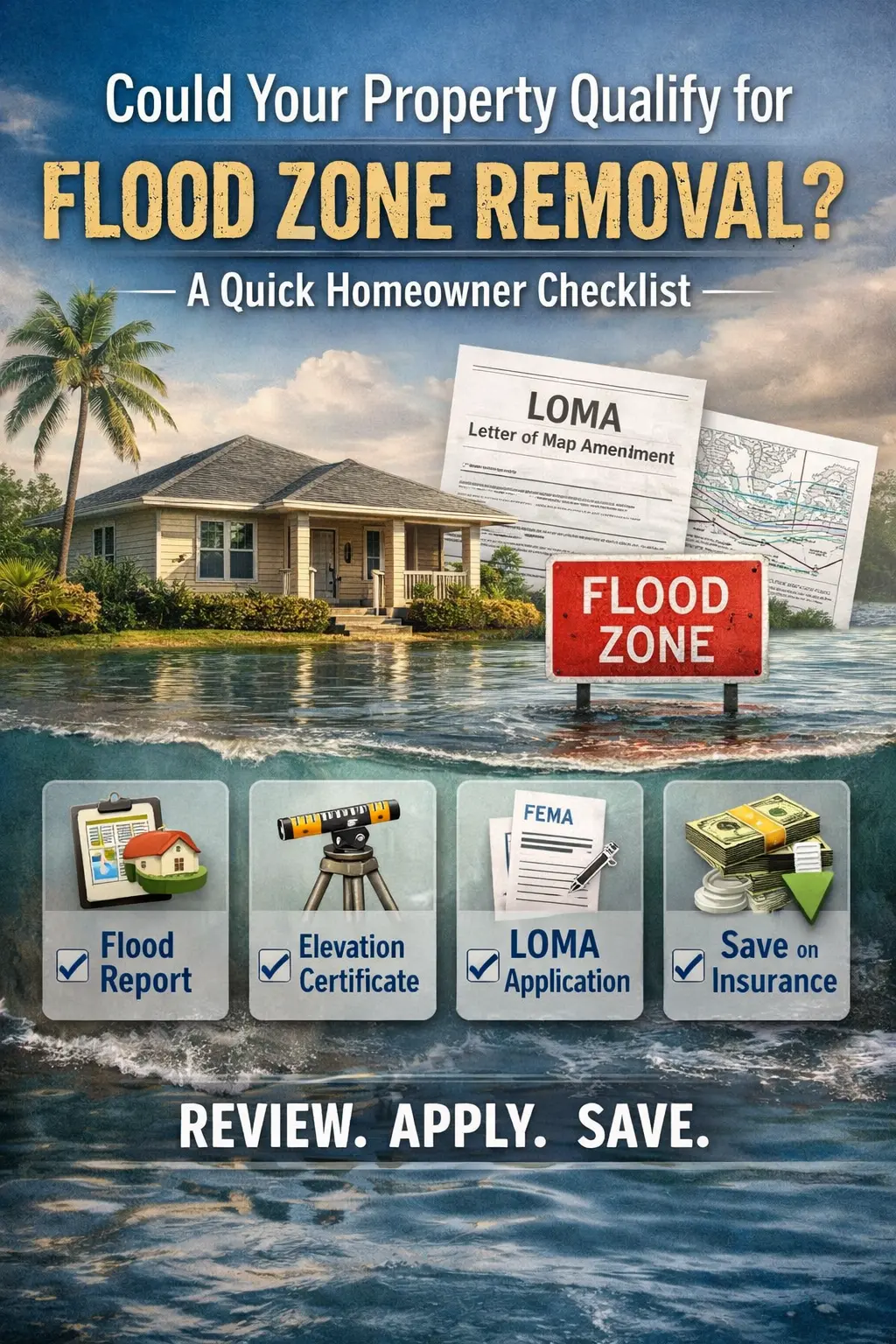

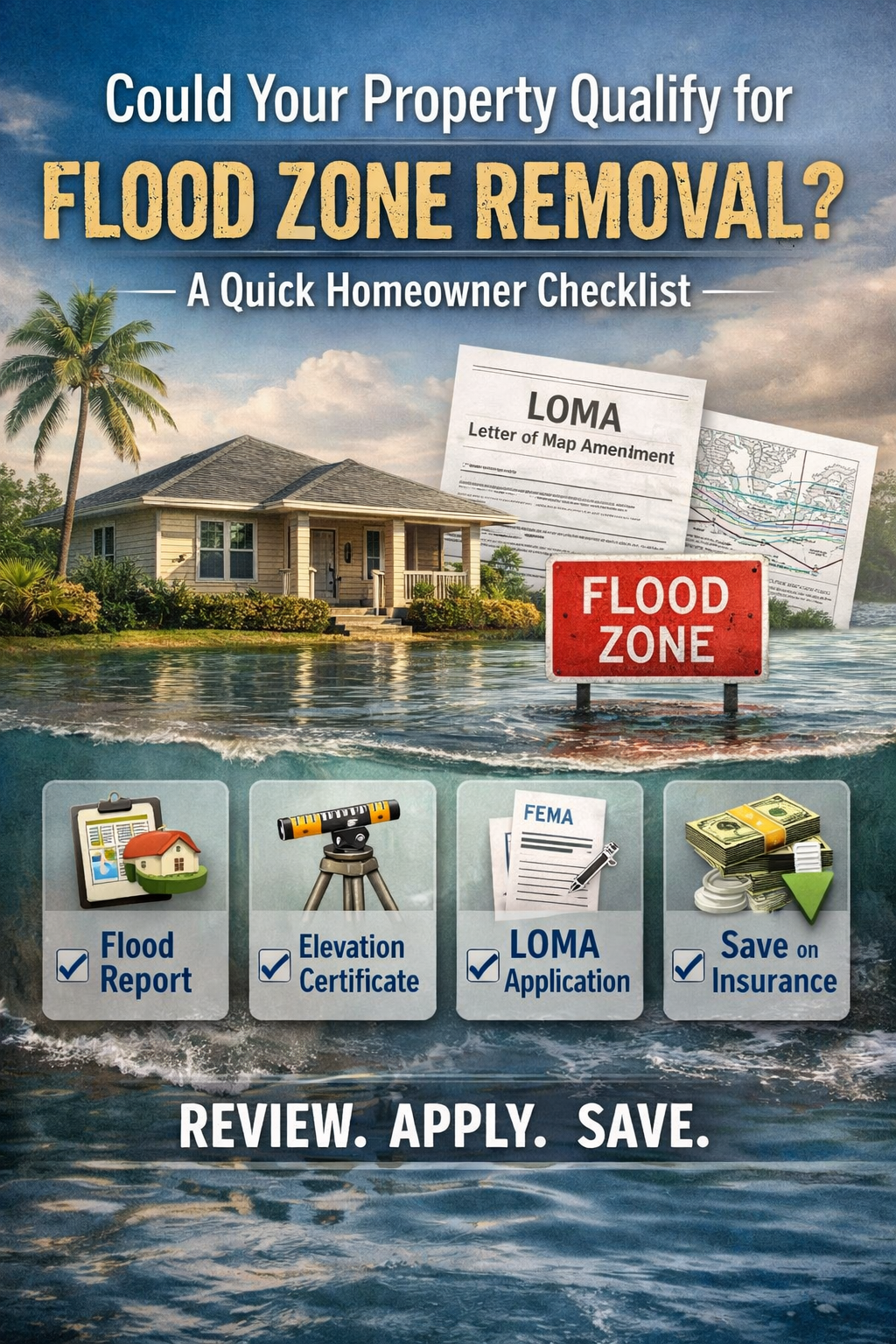

Could Your Property Qualify for Flood Zone Removal?

Could Your Property Qualify for Flood Zone Removal?

A Quick Homeowner Checklist

FLOOD ZONE. INSURANCE. OPPORTUNITY.

If you, your family or your friends own a home in Florida, chances are you’re either required to carry flood insurance by your lender—or it could be required it in the future, if your home becomes designated as being in a Special Flood Hazard Area (SFHA). Common SFHA designations include Zone A, AE, A1-A30, AH, AO, AR, V, or VE.

But here’s what many homeowners don’t realize:

- Your property may not actually belong in a flood zone

- It may affect the marketability of your home

- There is a formal process to challenge it

It’s called a Letter of Map Amendment (LOMA)—and it can be one of the most overlooked opportunities to reduce long-term homeownership costs.

The great news? We can help! See an overview of the process below, along with how you can contact us to get started. The sooner you start, the sooner you could start saving and improve your home's marketability 💵💰!

What Is a LOMA?

A Letter of Map Amendment (LOMA) is an official determination from Federal Emergency Management Agency (FEMA) stating that your home has been incorrectly mapped in a high-risk flood zone.

In simple terms:

- FEMA flood maps are not always precise at the individual property level

- Your home may sit above the Base Flood Elevation (BFE)

- If proven, FEMA can remove your property from the high-risk designation

If approved, this could mean:

✔ Elimination of mandatory flood insurance

✔ A significant reduction in premiums

✔ Increased marketability when selling your home

Why This Matters: Cost and Marketability Cost:

Flood insurance can be expensive—and costs continue to rise.

- Policies often range from hundreds to thousands per year

- Over 30 years, that can exceed $20,000+ in premiums

Note: In consulting with your insurance agent, you may still decide to carry flood insurance, but removing your home from a SFHA may result in a significant reduction in your flood premium.

Marketability:

- Being in a SFHA, may affect the marketability of your home - We have and do continue to receive feedback from buyer agents that their clients do not want to be in a flood zone. Here are some scenarios:

-

- First-time or limited budget buyers purchasing with home loans - Monthly flood insurance costs may disqualify them from buying at your list price but at the same price, they qualify for a non-SFHA home.

- Out-of-state buyers - Sometimes avoid flood zones due to recent hurricanes.

- Cost-conscious buyers - Controlling current and future costs where they can due to higher interest rates and the increasing cost of living.

The opportunity:

- Immediate reduction of hundreds to thousands of dollars per year

- Potential lifetime savings in the tens of thousands

- Lowers monthly payment for potential buyers and also gives them the option to purchase flood insurance versus it being required by their lender.

One of our goals is to help you maximize the sale price of your home. This is one of the rare scenarios in real estate where a relatively small upfront investment can produce substantial long-term ROI.

Why Most Homeowners Never Hear About This

This is where it gets interesting.

- Insurance companies rely strictly on FEMA maps—not property-specific elevation

- Lenders are required by federal law to enforce flood insurance in high-risk zones

- There is no incentive for insurers to suggest removing coverage

Which means…

Unless a knowledgeable advisor (like us), surveyor, or proactive homeowner brings it up—

this opportunity is often missed entirely.

Important Considerations

Even if a LOMA is approved:

- Your lender may still require flood insurance - A quick call to your agent should provide insight.

- Flooding can still occur outside mapped zones

- Approximately 25% of flood claims happen outside high-risk areas

This isn’t just about removing insurance—

it’s about making an informed, strategic decision.

A Quick Homeowner Checklist

Use this as a starting point to determine whether your property may qualify:

1. Start with a Flood Determination Report

- Confirms whether your structure is actually within a Special Flood Hazard Area (SFHA)

- Provides precise mapping and structure location

- Typical cost: ~$25 | Turnaround: 24–48 hours

Call or text us at 813-693-1003 to order this You may also Email us.

2. Get an Expert Review

A Certified Floodplain Manager (CFM) can:

- Identify if your property has been incorrectly classified

- Evaluate whether you may qualify for a LOMA

- Recommend next steps based on your specific property

We have contacts for this.

3. Obtain an Elevation Certificate (If Needed)

- Completed by a licensed surveyor

- Confirms your home’s elevation relative to flood levels

- Typical cost: ~$225–$300

We can recommend reasonably priced surveyors.

4. Submit a LOMA or eLOMA Application

Two primary paths:

- LOMA (Standard)

- Timeline: ~6–8 weeks

- Cost: ~$150

- eLOMA (Expedited)

- Timeline: 1–10 business days

- Cost: ~$400

The Bottom Line

If your home has been placed in a flood zone, it doesn’t automatically mean it belongs there.

And in many cases, homeowners who take the time to investigate:

- Reduce or eliminate insurance costs

- Strengthen their resale position

- Gain a clearer understanding of their property’s true risk

You may have a neighbor who has already successfully done this!

But, it’s not just about saving money—

it’s about uncovering an opportunity most homeowners never realize exists.

How We Can Help

If you’re curious whether your property may qualify, we can help guide you through the process—from ordering the initial flood determination to connecting you with trusted local experts to quickly move through the process. Take 5 minutes and call us to get started today. The sooner you start, the sooner you could start saving 💵💰!

📞 813-693-1003

📧 uppertampabay@evrealestate.com

A conversation. Not a sales pitch. Our job isn't to sell, it's to help people.

Categories

- All Blogs (294)

- About the E&V Brand (2)

- Buying in Tampa Bay (3)

- Buying Real Estate (10)

- Florida (5)

- Fun Things To Do in Tampa Bay (1)

- Holidays (2)

- Homeowner Hacks & Tips (2)

- Important Info (11)

- Lifestyle/Wellness (5)

- Selling in Tampa Bay (1)

- Selling Real Estate (11)

- Tampa Bay Real Estate & Beyond (14)

- Working with EV Upper Tampa Bay (8)

Recent Posts